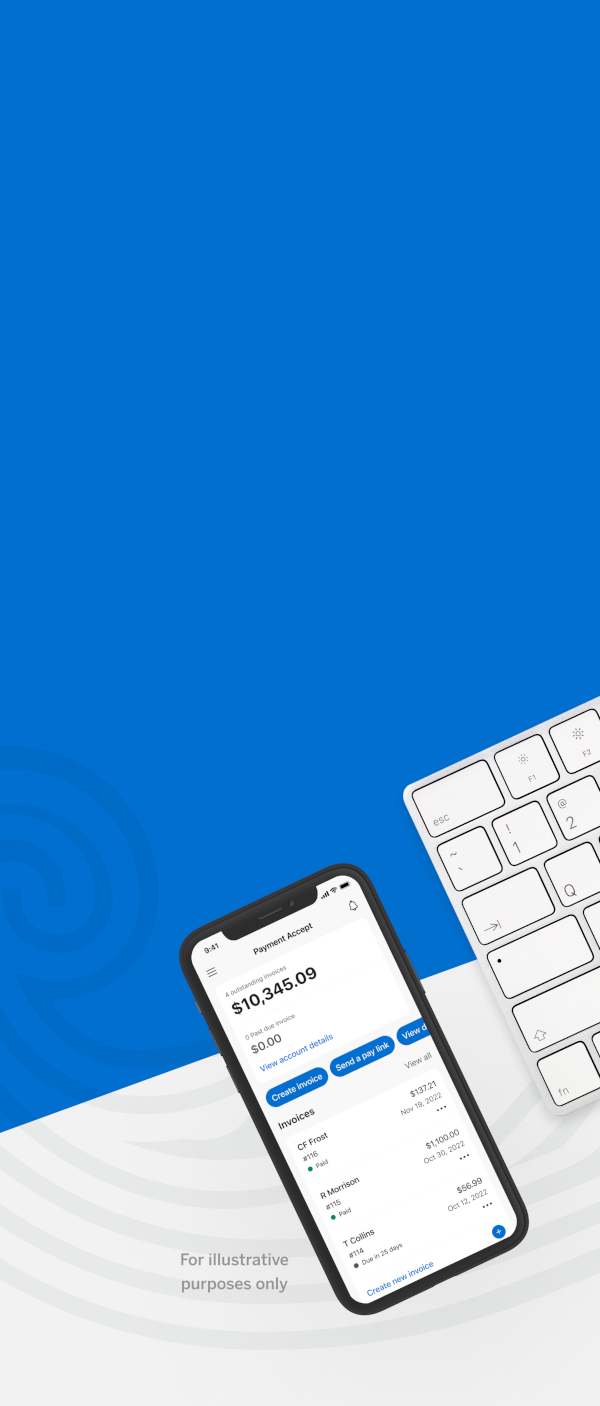

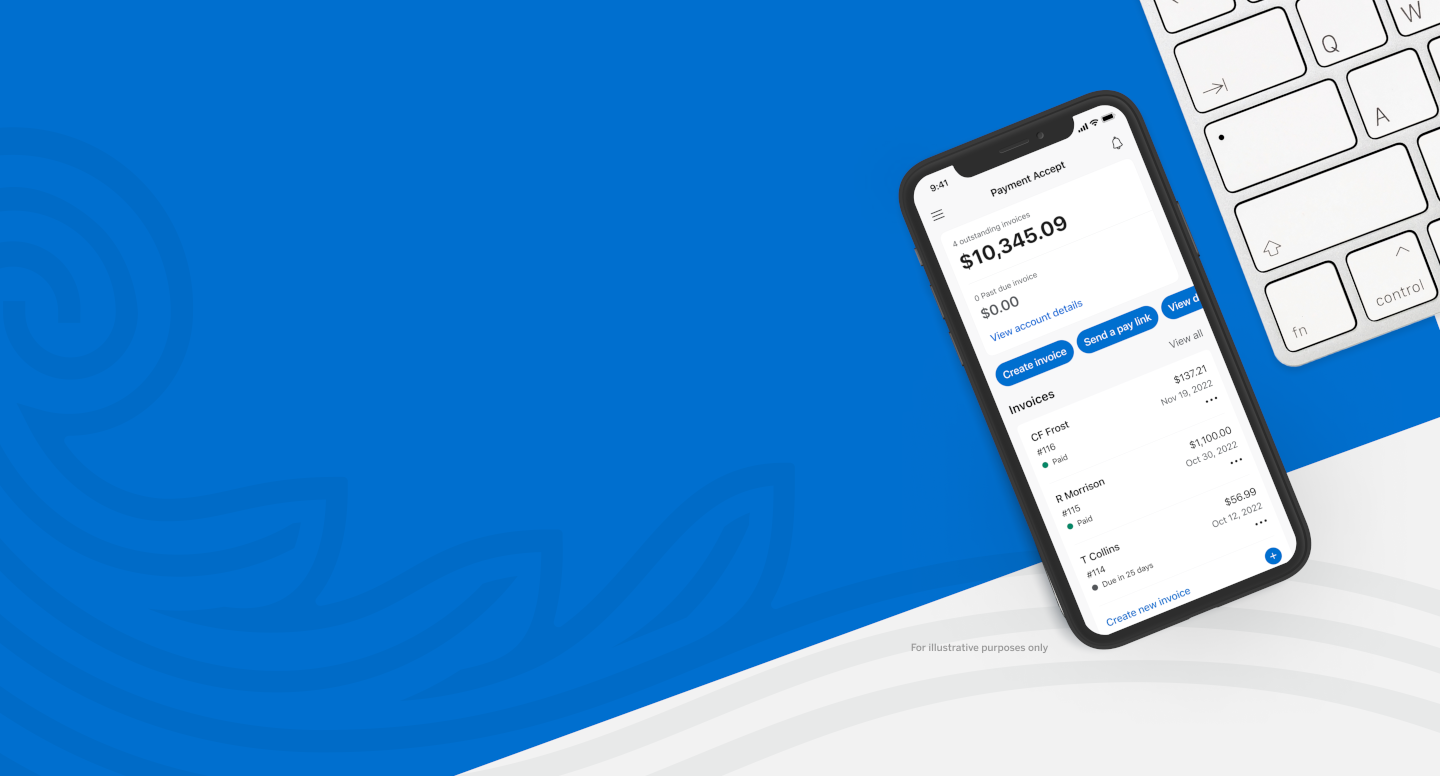

Thank you for your interest in American Express® Payment Accept.

Payment Accept is not accepting new customer applications at this time. Current Payment Accept customers, you can continue to log in to access your account. For more information about this product, visit the help center.

Designed to support businesses like yours, American Express Business Blueprint™ is a free platform that gives you insight into how money moves in and out of your business, so you can make more confident cash flow management decisions.

Explore more

Check out these products designed to help you run your business

American Express® Business Line of Credit

Focus on growth with flexible access to business funding.‡

Learn more

American Express® Business Checking

Earn 1.30% APY4 on balances up to $500,000. Terms apply. Member FDIC.

Learn more

American Express Business Blueprint™

View your select business products and accounts5 in one place.

Learn more